About RiskSkill’s e-Money Compliance Services

RiskSkill help businesses avoid €multi-million fines and embarrassing brand damaging mistakes from regulatory non-compliance and process and regulatory mistakes. We help clear up the mess when we are called in later.

E-money Licence Changes:

Recent new financial services legislation in the UK, has led to the Financial Conduct Authority (FCA) introducing a Payments Systems Regulator from April 2014. The ECB, and the European Commission are also proposing ways to regulate and police the whole e-money arena, as are the international card schemes. The FCA is now also starting to review and audit the e-money licences they have granted previously and for observance with ALL regulations and also best-practices.

We believe that the FCA have seen that the governance of payment systems, including e-money issuers, is a difficult and continuous task and needs several layers of supervision and oversight in the way that other payment methods have already established (e.g. through the regulations of the international card schemes).

Requirements:

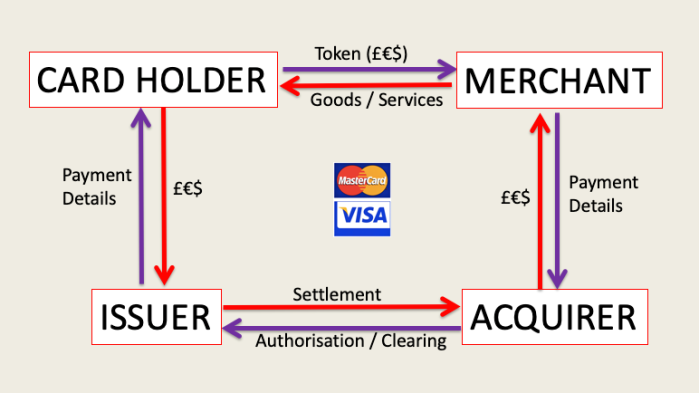

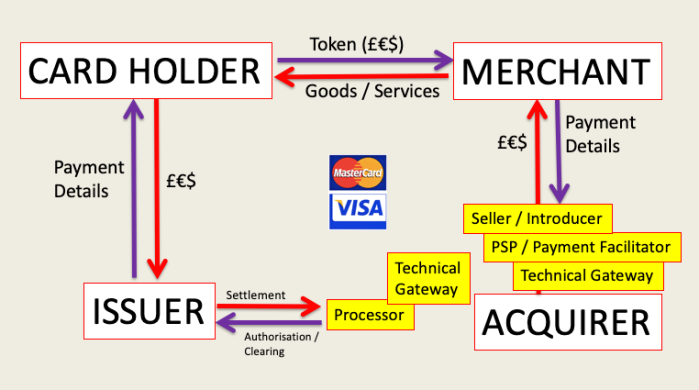

As an e-money licence holder, you need to ensure that your organisation and all of its agents, including passport holders, are fully conversant with and engaged in all due diligence in customer selection and identification, transaction/event screening, suspicion reporting, record-keeping, corporate assessment of exposures and risk, and the Base II (and III) capital assignment to the exposures. Having reporting to the FCA, a clear payment strategy and ABOVE ALL understanding and observance of laws relating to payments in all areas of operation are all also essential.

The main legislation that is pertinent is the meeting of the requirements of the Money Laundering regulations for all countries in which an e-money licence holder, and its agents and Passport Holders, operates. Not doing what is right by the European Money Laundering directives is the quickest way of losing money, being fined, suffering crippling bad media attention, or losing a market – or a full e-money licence (which will happen when firms are reviewed).

ACTIONS

In advance of the FCA performing its own validation on individual license holders (and making high profile examples of those who are not fully compliant), you need to:

A. Make sure that all your processes, operations and compliance teams are all fully observant of all applicable regulatory requirements, laws and best practices.

B. More importantly though, are you confident that your third party agents are also fully compliant?

We Can and Will Help You In:

1. Determining your current state of preparedness and identify areas for attention and action before the FCA requests an onsite review of your business.

2. Review the state of compliance and preparedness of your third party agents or passport-licences and report to you on them as the principal e-money licence holder?

We can provide you with our credentials when you need help, as we are a team of payment industry specialists, that have previously worked in many banks and card schemes, and now help organisations assess their current operational status, and become and remain compliant. We have also worked extensively with the rules, regulations, legislation and best practice across the sector, in the UK and across Europe and advise payment organisations on market strategy and direction rather than simply focusing on ‘tick-box’ auditing.

Contact RiskSkill for our Services for all Risks, Fraud and Compliance solutions for e-money, e-payment, internet payments, e-funds, e payment systems, online payment and digital cash’s safe transactions. RiskSkill is also a permanent member of AIRFA an independent and global risk and fraud advisors organization.

Bill Trueman is a professional banker and a payments and risk specialist, with over 25 years of experience. He headed-up risk functions and special investigations in Lloyds Bank issuing and acquiring; acquiring and processing at First Data, and then for insurance risks at RBS / Direct Line. For the last 12 years he has been diving-into many other businesses: largely advising merchants, acquirers and others in the payment chain; to reduce risks and costs, and to find improved ways to do business and/or to make significant organisational change. He is a mentor for innovative payments startups and sits on working parties and panels for the UK regulators.

Bill Trueman is a professional banker and a payments and risk specialist, with over 25 years of experience. He headed-up risk functions and special investigations in Lloyds Bank issuing and acquiring; acquiring and processing at First Data, and then for insurance risks at RBS / Direct Line. For the last 12 years he has been diving-into many other businesses: largely advising merchants, acquirers and others in the payment chain; to reduce risks and costs, and to find improved ways to do business and/or to make significant organisational change. He is a mentor for innovative payments startups and sits on working parties and panels for the UK regulators.